Skip to main content

Top Navigation

Return to AUASB.gov.au

Latest news

Visit the Archive

Main navigation

Search

Menu

Recently issued standards

Auditing Standards

Sustainability Assurance

Review Engagements

Assurance Engagements

Related Services

Guidance Statements

Recently issued standards

Auditing Standards

Sustainability Assurance

Review Engagements

Assurance Engagements

Related Services

Guidance Statements

Home

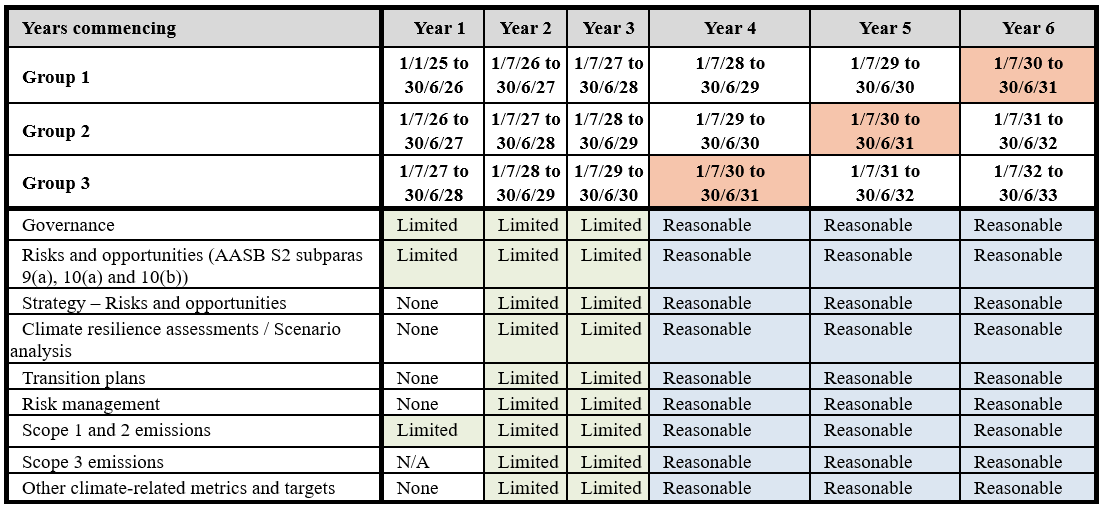

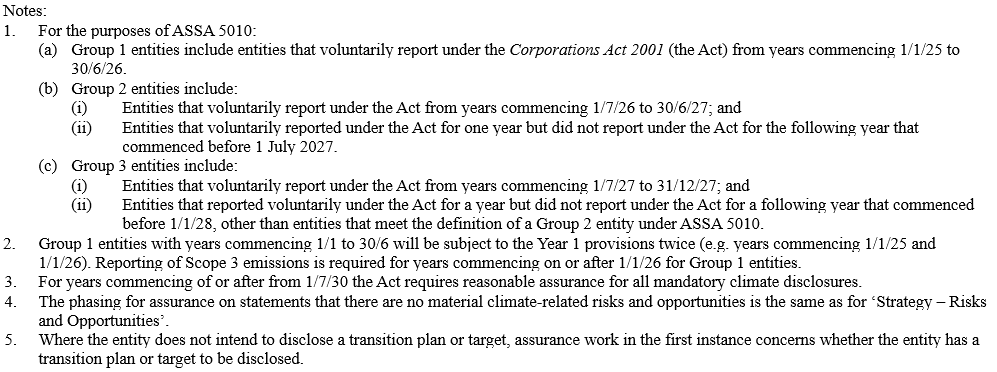

Appendix (ASSA 5010 January 2025)

Appendix - Diagrammatic representation of assurance phasing

(Ref: Para.

10

)

Top of Page